For many homeowners, equity can be a practical way to step into property investment without…

The ultimate guide to small homes and granny flats

With property prices climbing steadily across Australia, the dream of homeownership looks very different today than it did a generation ago. For many, large suburban blocks or sprawling family homes are out of reach — and out of step with their lifestyle.

This is where small homes and granny flats have stepped into the spotlight.

From first-time home buyers searching for a lower entry point to retirees wanting to downsize or families seeking rental income, small homes offer a practical alternative to traditional housing.

But like any major decision, they come with both opportunities and challenges. This guide unpacks everything you need to know about small homes, modular builds, granny flats, and capsule housing. We’ll explore:

- The pros and cons

- Financial strategies

- Local council approval requirements across Newcastle, Maitland, Cessnock, and Singleton.

What is a small home?

A “small home” is generally considered a dwelling under 100 square metres. That said, size can vary depending on design, location, and purpose. In recent years, demand has grown for a wide range of smaller housing options, including:

- Granny flats – Secondary dwellings built on the same lot as a primary residence. They can be attached, detached, or within the main home.

- Modular homes – Prefabricated sections constructed in a factory and assembled onsite. These can be full-sized homes or smaller modular granny flats.

- Tiny homes – Ultra-compact dwellings, often under 50 square metres, sometimes built on trailers for mobility.

- Kit/capsule homes – Delivered as pre-cut materials or factory-built capsules, offering cost-effective solutions with varying levels of customisation.

Each format appeals to different buyers, from those chasing affordability to investors seeking long-term returns.

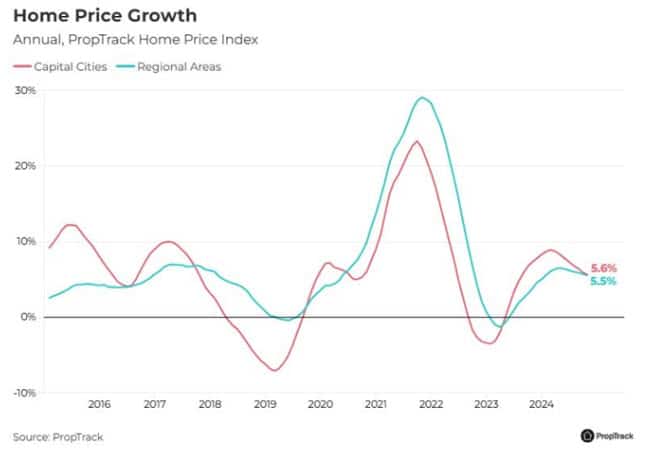

Why small homes are becoming more popular in Australia

The allure of regional Australia has grown significantly as remote work becomes more viable and accepted. Costs to live in capital cities have become unattainable for a lot of Australians, which is why cities like Geelong, Ballarat, and Newcastle are seeing an influx of new residents seeking more affordable housing options, larger lot sizes, and a perceived better quality of life away from urban congestion.

This migration is boosting local economies and reshaping property demand patterns.

Here are some extra statistics to put things into perspective:

- Over 538,000 new home construction commencements over the past 3 years

- 13% increase in volume of Real Estate transactions from last year

- 117,000 properties purchased by first-home buyers (9% more than the previous year).

Pros of buying a small home

Image: Freepik

Buying a smaller property has various financial, practical, and lifestyle advantages.

Affordability

|

Lower maintenance

|

Energy efficiency

|

Faster build times

|

Flexible living arrangements

|

Lifestyle shift

|

Resale advantages

|

Cons of buying a small home

Image: Freepik

Of course, small homes aren’t the perfect solution for everyone. It’s important to weigh the downsides carefully.

Limited space

|

Resale challenges

|

Council regulations

|

Design limitations

|

Potential for overcrowding

|

Hidden costs

|

Vacancy risk (for granny flats)

|

Deep dive comparisons

Granny flatsGranny flats are one of Australia’s most popular small home options, offering flexibility and financial benefits. Advantages of granny flats

Drawbacks of granny flats

Costs and timelines

Living trends

|

Modular and capsule homesModular and capsule housing has grown in popularity thanks to affordability and sustainability. Advantages of modular and capsule homes

Drawbacks of modular and capsule homes

Costs

|

Financial scenarios & case studies

One of the biggest advantages of granny flats or modular additions is their financial potential.

Case study #1: Buying a home with space for a granny flat

- Home value: $885,000

- Loan balance: $585,000

- Add a granny flat for $120,000

- Rent granny flat at $300 per week

In this case, the loan impact would be:

- Repayments on $120,000 at 5.64% over 30 years = $152/week.

- Rental income = $300/week, leaving $148 surplus.

- Extra repayments reduce the primary mortgage term by 9.3 years.

- Total savings: over $200,000 in repayments.

This example highlights how small homes can accelerate wealth creation and mortgage reduction when structured correctly.

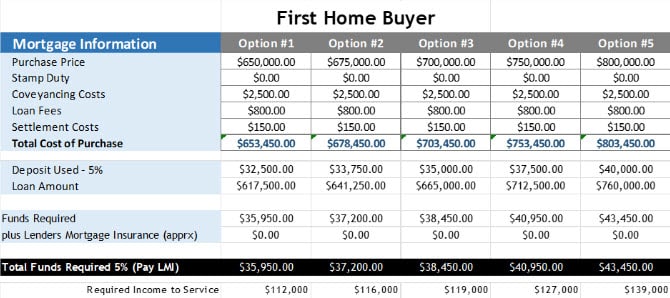

Case study #2: First-home buyers

A quick guide to council approval and regulations in NSW

Understanding the approval process is critical before committing to a granny flat, modular home, or tiny home. Before we dive into approvals with the Newcastle, Maitland, Singleton, and Cessnock Councils, there are three terms you need to know:

- Exempt Development – Very minor works that meet strict criteria, no approval needed.

- Complying Development Certificate (CDC) – A fast-tracked approval for low-impact builds.

- Development Application (DA) – Full council assessment for more complex projects.

Newcastle City Council

|

Maitland City Council

|

Cessnock City Council

|

Singleton Council

|

Council approvals can be complicated and time-consuming, but here are some pro tips for making the process simpler:

- Engage early with council duty planners.

- Use the NSW Planning Viewer to confirm zoning.

- Prepare thorough documentation (site plans, drainage, elevations).

- Incomplete applications are the most common cause of delays.

- Consider professional town planning or certification support.

Choosing a small home or adding a granny flat is more than a financial decision—it’s a lifestyle choice

The benefits of affordability, flexibility, and sustainability need to be balanced against limitations like space, resale potential, and regulatory hurdles.

If you’re considering financing a small home, building a granny flat, or exploring modular housing, Watson Mortgages can help—our team partners with over 30 lenders to compare loans, interest rates, and terms. We’ll present options that fit your financial situation and property goals — at no cost to you.

Whether you’re a first-home buyer, investor, or looking to downsize, we’ll make the process simple. Contact us today to explore your options!

Disclaimer

Watson Mortgages Pty Ltd (Nestor Ramirez Credit Representative Number 378816 and Gary Gilbert Credit Representative Number 432216) is authorised under Australian Credit Licence 389328.

Watson Mortgages Pty Ltd ABN 29 642 538 967 is a separate entity to Elliot Watson Financial Planning Pty Ltd. Elliot Watson Financial Planning Pty Ltd is a Corporate Authorised Representative of RI Advice Group Pty Ltd, ABN 23 001 774 125 AFSL 238429.

This article provides general information only and has been prepared without taking into account your objectives, financial situation or needs. We recommend that you consider whether it is appropriate for your circumstances and your full financial situation will need to be reviewed prior to acceptance of any offer or product. It does not constitute legal, tax or financial advice and you should always seek professional advice in relation to your individual circumstances.

Article by Gary Gilbert – Senior Mortgage Broker

Relevant Articles